Anthropic Today,

profitability, IPO, and the heavy user's seat

The series began inside a small office of one company. Seven episodes later, it closes by returning to where that company stands today. In the spring of 2026: the first frontier-AI company reported to reach a quarterly operating profit, a $900B round under review, and the most-cited IPO candidate in this cycle. And one heavy user's view of Claude. The actual closing chapter of the series.

Coming back to where we began

This series began with a single company's founding story. The room in San Francisco in December 2020 where Dario and Daniela Amodei decided to leave OpenAI. Six episodes later, we gathered the six answers being written across the same industry and gauged five years forward in three scenarios. The reason this series carries the name An Anthropic Story, however, is that one of those six seats is where the series began. The closing chapter has to return to that seat for the series to actually close.

Looking at it from spring 2026, that seat is distinctly different from the other five. First, the revenue curve is different. Q1 revenue of about $4.8 billion to Q2 expected revenue of about $10.9 billion — roughly 130% growth quarter over quarter. Second, this is the first frontier-AI company reported to reach a quarterly operating profit. Third, it is most often cited as the next major IPO candidate. Fourth, the round under review at the same moment values the company at about $900 billion, above OpenAI's current valuation per reports. Last, it is the company that, almost single-handedly, occupies the "safety identity" seat in this industry.

This essay walks through those five seats one by one. At the end, one more thing is added. The editor writing this essay is, day to day, a heavy user of Claude. The angle of looking at a company from the outside is not the same as the angle of holding that company's tool in your hand every day. The closing chapter is where those two angles meet.

Spring 2026 — Anthropic's coordinates

Let us first place the coordinates of right now on a single page. Q1 2026 revenue: approximately $4.8 billion. Bloomberg's May 20 report and CNBC's same-day piece point at the same number. Q2 2026 expected revenue: approximately $10.9 billion, per those same reports. Quarter-over-quarter growth of roughly 130%. A slope you do not often see on a revenue chart.

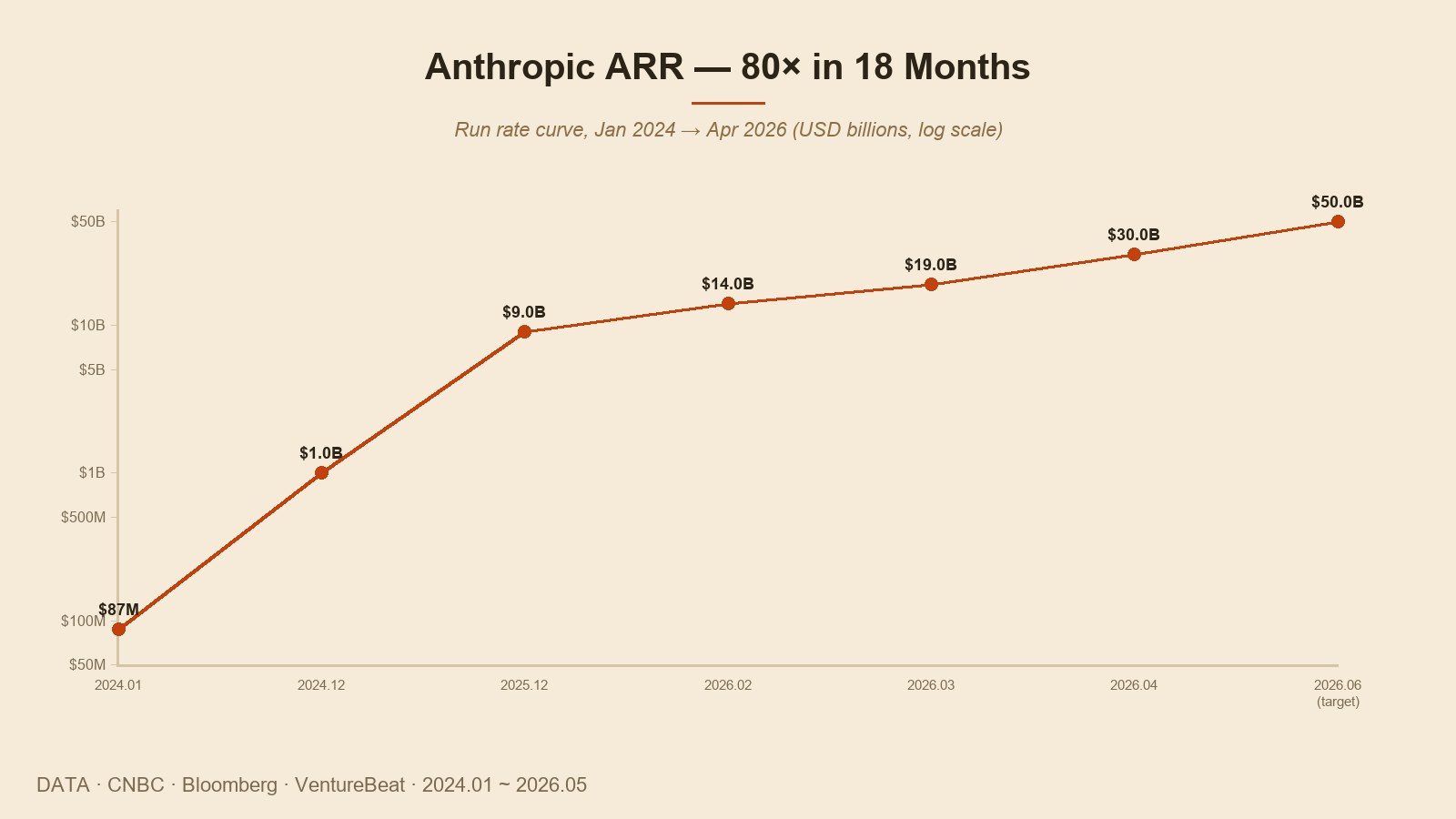

The longer ARR (annualized run rate) curve makes the steepness even clearer. About $87 million in January 2024. About $1 billion in December 2024. About $9 billion at the end of 2025. About $14 billion in February 2026, $19 billion in March, and approximately $30 billion in April. The company has guided to a run rate around $50 billion by the end of June 2026. Roughly 80-fold growth in about 18 months. Inside the company that curve has reportedly picked up a nickname: "the crazy 80x."

What is driving this revenue? One pattern stands out. Enterprise and API. The consumer chatbot tiers (Claude.ai's free, Pro, and Max lines) are also growing, but the steepness of the curve comes from business customers. Per the reports, more than 1,000 enterprise customers are now spending over $1 million per year with Anthropic, and many of them have integrated Claude deeply into their own products — code assistance, call-center automation, legal document review, medical chart processing, and similar use cases.

Workforce is another coordinate. From about 800 employees in spring 2025 to about 1,500 in spring 2026. Roughly doubled in a year. For comparison, OpenAI is in the ~3,000 range, xAI in the ~1,200 range. Anthropic is one of the highest revenue-per-employee companies among the frontier names. This one line is the central variable behind the profitability story in the next chapter.

Profitability — the only case among frontier AI

At the end of this curve, one more joint appears. Anthropic is on track to reach its first quarterly operating profit in Q2 2026. CNBC's May 20 report and Bloomberg's report from the same date cite the same source: about $559 million in operating profit against $10.9 billion in revenue. Among the frontier AI companies, Anthropic is the only one with reporting like this in this cycle.

Over the same period, OpenAI is reported to be running a large operating loss against approximately $15 billion in revenue — the most-cited figure puts the 2025 annual loss at over $5 billion. xAI does not disclose detailed revenue and is widely assumed to be running a large loss given infrastructure capex. Meta's and Google's AI lines fold into parent P&Ls and cannot be separately tracked. Mistral is at a different stage entirely. "A frontier AI company has reached quarterly operating profit" is a sentence this industry is hearing for the first time in spring 2026.

How did this happen? Two variables. First, the 80x revenue growth outran cost growth. Revenue grew faster than inference cost and headcount cost. Second, the revenue mix is heavily enterprise and API. Unlike consumer models (ChatGPT's free tier and the like) where inference cost from free users has to be offset by ads or other revenue, most of Anthropic's revenue sits on usage-based contracts. Each GPU hour converts to revenue more directly.

Two caveats deserve to be marked. First, these figures are unaudited, non-GAAP estimates, as the same reports explicitly state. Once the IPO process begins, GAAP reconciliation may shift some numbers. Second, one profitable quarter is not a guarantee of sustained profitability. The same company continues to spend on the order of tens of billions per year on training the next models. "The first frontier company where revenue caught up to capital" is a strong sentence, but it is not a promise about the future.

PBC — structural firmness

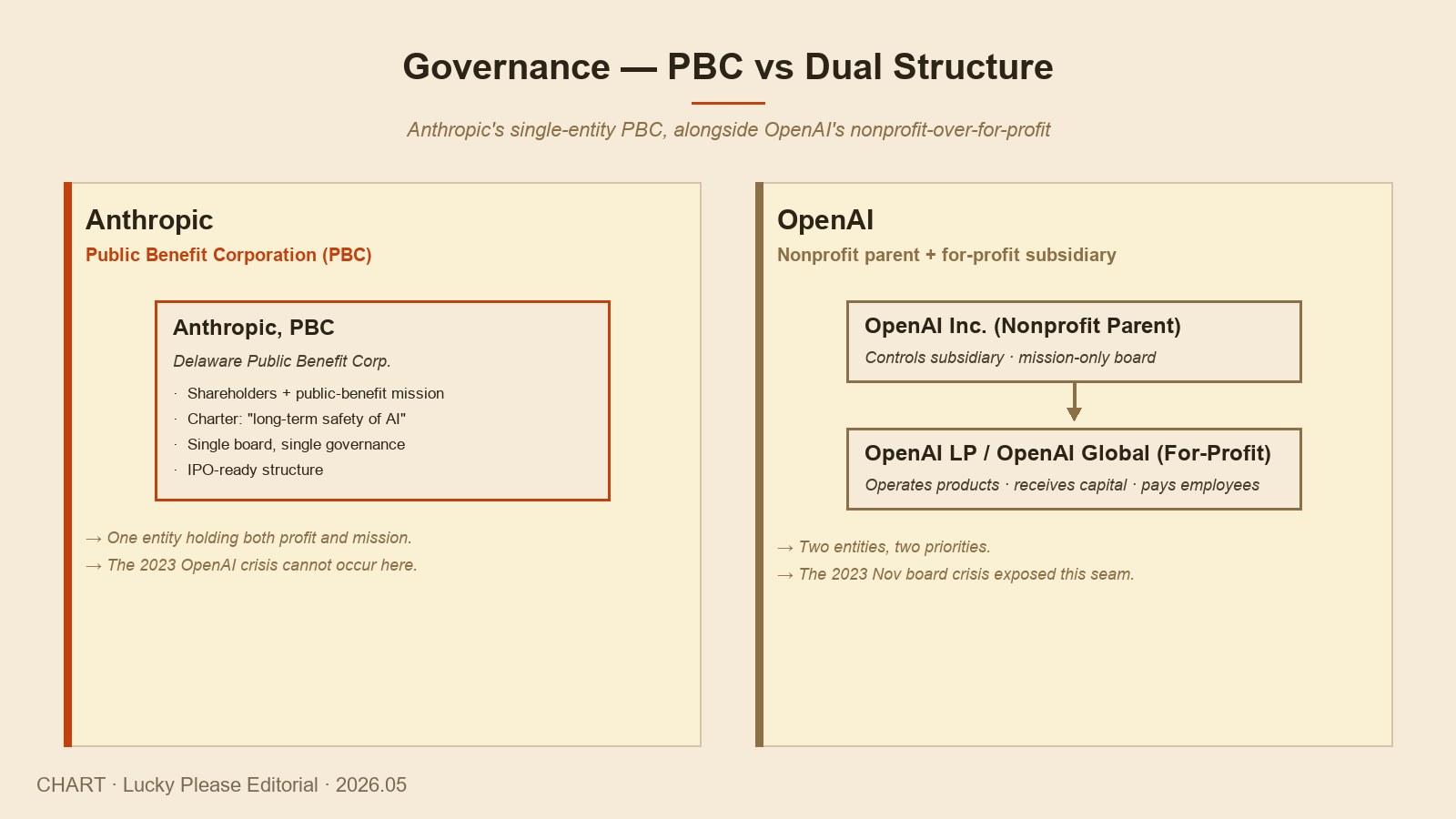

One more thing makes Anthropic's seat thicker — the structure of the company itself. Public Benefit Corporation (PBC). A specific kind of for-profit incorporated under Delaware law. It carries the same for-profit responsibilities as a C-corporation, while also bearing an obligation to pursue a public-benefit purpose written into the charter. Anthropic's stated purpose, in one line: "the responsible development and maintenance of advanced AI for the long-term benefit of humanity."

What difference does this make? Setting it next to Ep.4's "Five Days of Crisis" makes it sharper. The November 2023 OpenAI crisis was a one-time exposure of the awkwardness inherent in a nonprofit parent (OpenAI Inc.) abruptly removing the CEO of its for-profit subsidiary (OpenAI LP). Those five days showed the industry what can happen when nonprofit mission and for-profit operation lose balance inside a single company spread across two entities.

Anthropic's PBC structure does not split the two. Mission and for-profit responsibility live inside the same legal entity. Governance becomes simpler. The relationship between CEO and board does not get murky, and when shareholder interest collides with mission, the collision is processed inside one entity's self-balance. The simplicity is also a major advantage in the IPO process: SEC disclosure obligations, shareholder accountability, and mission consistency can all be reconciled in one place.

This structure produces one more effect. The company's identity does not wobble. Anthropic has held the same single-line identity, "long-term safety of frontier AI," for five years. The Constitutional AI training approach, the staged evaluation under the Responsible Scaling Policy, the pre-review process with external evaluators — all of it flows from a duty embedded in the charter rather than from year-to-year corporate choice. That is a clear contrast with OpenAI's drift from nonprofit to capped-profit to something approaching a full for-profit company across the same period.

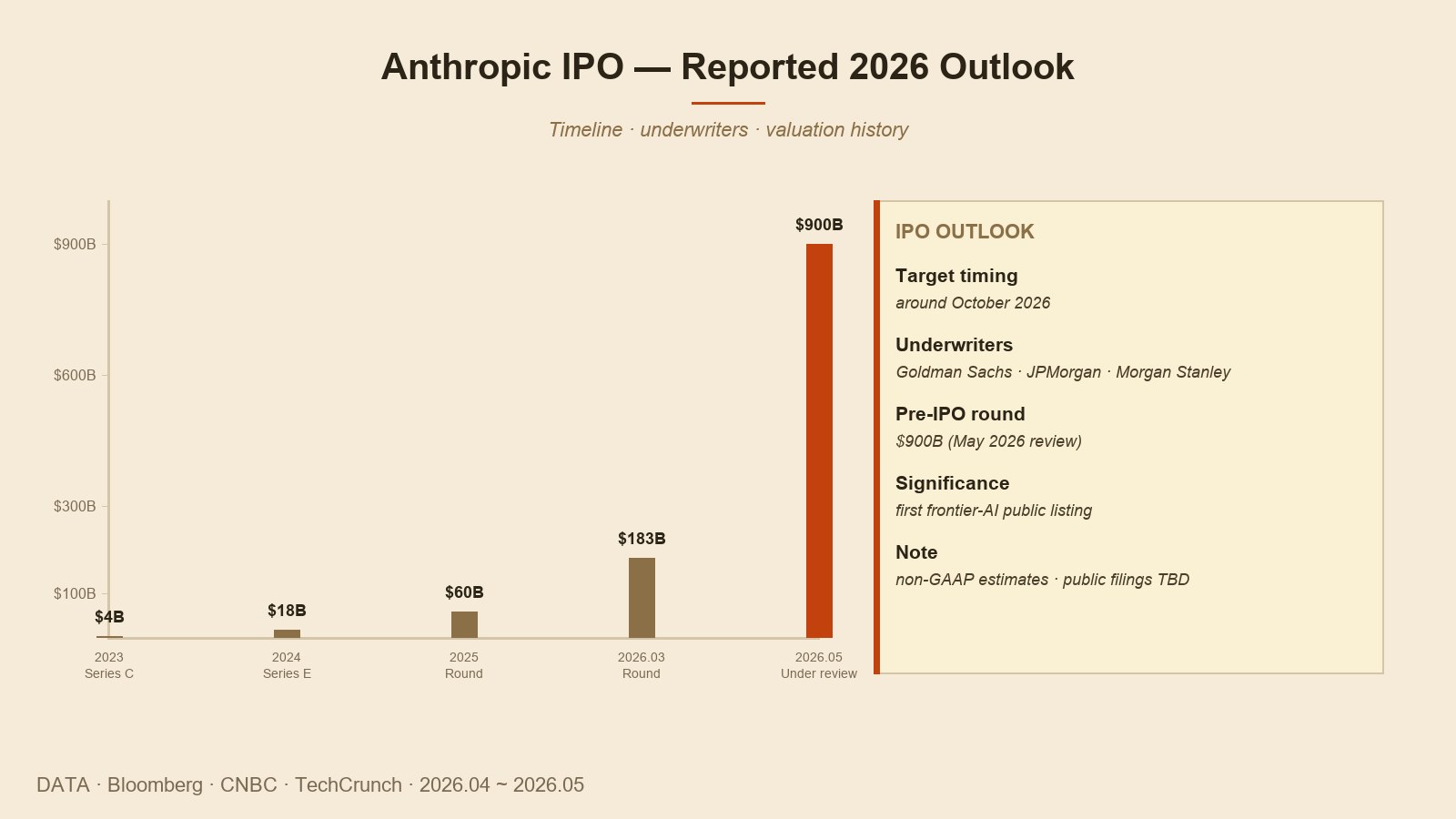

IPO — the seat in October 2026

All of these coordinates converge on one place: IPO. As of spring 2026, the most-cited scenario is around October 2026. Goldman Sachs, JPMorgan, and Morgan Stanley are reported in early discussions as underwriters in May. The same period's funding round under review is valued at approximately $900 billion — above the most-cited valuation for OpenAI (in the ~$500 billion range).

If that IPO happens, one seat in the industry settles. The first frontier AI company to enter the public market. OpenAI cannot move quickly given the structural complexity discussed above. xAI is still inside its private funding cycle. Google's and Meta's AI lines are folded into parents. So the first channel through which a general public investor can directly hold equity in a frontier model company would be Anthropic's IPO. That fact, more than the valuation number itself, is what carries the larger meaning.

A few caveats remain. First, the $900 billion is the valuation of a round under review, not an actual public-market price. The market capitalization at the time of listing may differ. Second, if the revenue curve steepness does not hold, post-listing volatility may be high. Whether ARR growth from $5B to $30B in roughly 18 months continues in the same shape over the next one or two years is not knowable in advance. Third, against the industry-wide picture of capex still running ahead of revenue, whether a single company's profitability settles into a sustained shape depends on several variables aligning.

One note for Korean and Asian retail investors. If Anthropic's IPO is conducted in the US, direct buying would proceed via an NYSE or NASDAQ listing through a US brokerage account. Indirect exposure during the pre-IPO window exists in pieces (Amazon's stake, Google's stake, certain AI ETFs), but the weight of that exposure varies by holding. This essay carries no buy or sell recommendation. What it does report is that the clearest IPO signal in spring 2026 sits at Anthropic, which means the name will be one Korean investors will meet most often in the coming year.

The heavy user's seat — from where Claude is used

The previous four chapters looked at the company from the outside. This chapter shifts the angle. This is a record from one of the editors who uses Claude as a daily heavy user — what it actually feels like to hold this tool in hand and work with it. The angle of analysis and the angle of daily use are different, so the tone of this chapter may sit slightly differently than the others.

The most-used tool is Claude Code. A command-line tool called directly from the terminal, where reading files, editing files, and running commands all flow inside a single conversation. The tool carries hooks — automation entry points where the model can be set to take certain actions at specific moments — and a "plan mode," a step where the model first lays out its plan before making real changes and waits for the user's confirmation. Those two together let the model's autonomy and the user's control balance in the same place. Compared with other AI coding tools, the simplicity of that balance is what stands out most clearly.

The second most-used place is Artifacts. When you ask for code, a document, or a chart inside a chat, the result does not just sit inside the conversation. It opens in a separate panel on the right side of the screen. There it runs, gets edited, and gets previewed. The flow of producing something in one place and refining it in the same place is one of the clearest differences from other chatbots.

And then there is the 1-million-token context window. For the work on this entire series, this one line was the decisive variable. Across six episodes of about 8,000–10,000 characters each, in four languages simultaneously, all of that text plus the figure guidelines plus the reference materials could sit inside one context together. Holding the tonal consistency of the series across the episodes without re-establishing it each round became possible largely because of the size of that context. The same volume of work would have been effectively impossible inside the 200K-context environment of a year ago.

Drawbacks exist too. Occasional response latency. Ambiguity of answers in certain domains. Quick exhaustion of free-tier limits. Claude Max's around-$200/month price is not a light price. These show up from the user's seat. But viewed through the lens of "a tool that has come to live inside the breath of daily work," the value Claude delivers in spring 2026 is not easily compared to any other frontier model in the same place.

Identity — what Constitutional AI and the RSP built

One variable that has set Anthropic apart from the other five is identity. For five years the same single-line identity: "long-term safety of frontier AI." That line sits in the charter, and from that charter line it flows out into nearly every part of how the company operates.

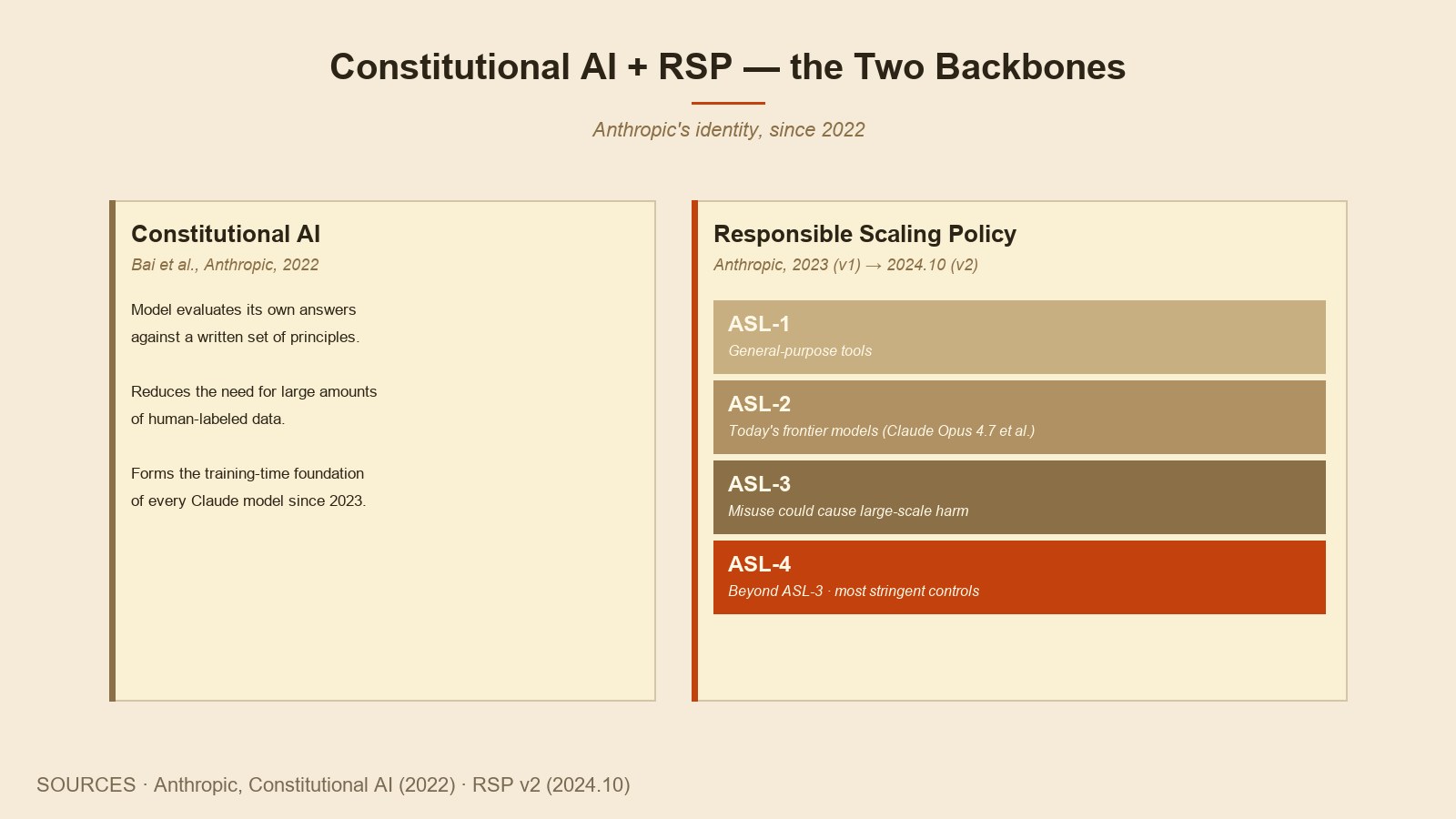

The two backbones of that identity are Constitutional AI and the Responsible Scaling Policy. The first is the training-time backbone, the second is the release-time backbone. Constitutional AI, introduced in a 2022 paper, is a training procedure in which the model evaluates and revises its own answers against a written set of principles — not relying solely on human labels, but applying the principles to itself. Every Claude model up to 2026 has been trained on a variation of that method.

The second backbone, the RSP, splits model risk into four tiers as noted above. ASL-1 is a general-purpose tool tier. ASL-2 is where most of today's frontier models sit. ASL-3 is a tier for models whose misuse could cause large-scale harm. ASL-4 sits beyond that. Each tier carries specific procedures: prior evaluation, external review, deployment restrictions. Before a new model is released, the company performs that tier's evaluation and discloses the result externally. OpenAI maintains an equivalent framework under the name "Preparedness Framework," and Google DeepMind under the name "Frontier Safety Framework," and both of those frameworks have publicly acknowledged Anthropic's RSP as a model they built on. The company that set the safety regimen standard is Anthropic.

How does this identity get received in the market? One clear seat: the enterprise market. Large customers in finance, healthcare, law, and government weigh the safety framework the model runs inside as heavily as accuracy or speed when making decisions. Where compliance and audit matter, even more so. The steepness of Anthropic's revenue curve, sourced from the enterprise mix, owes one of its biggest variables to the credibility of this identity. "A strong model run responsibly" lives directly inside the revenue curve.

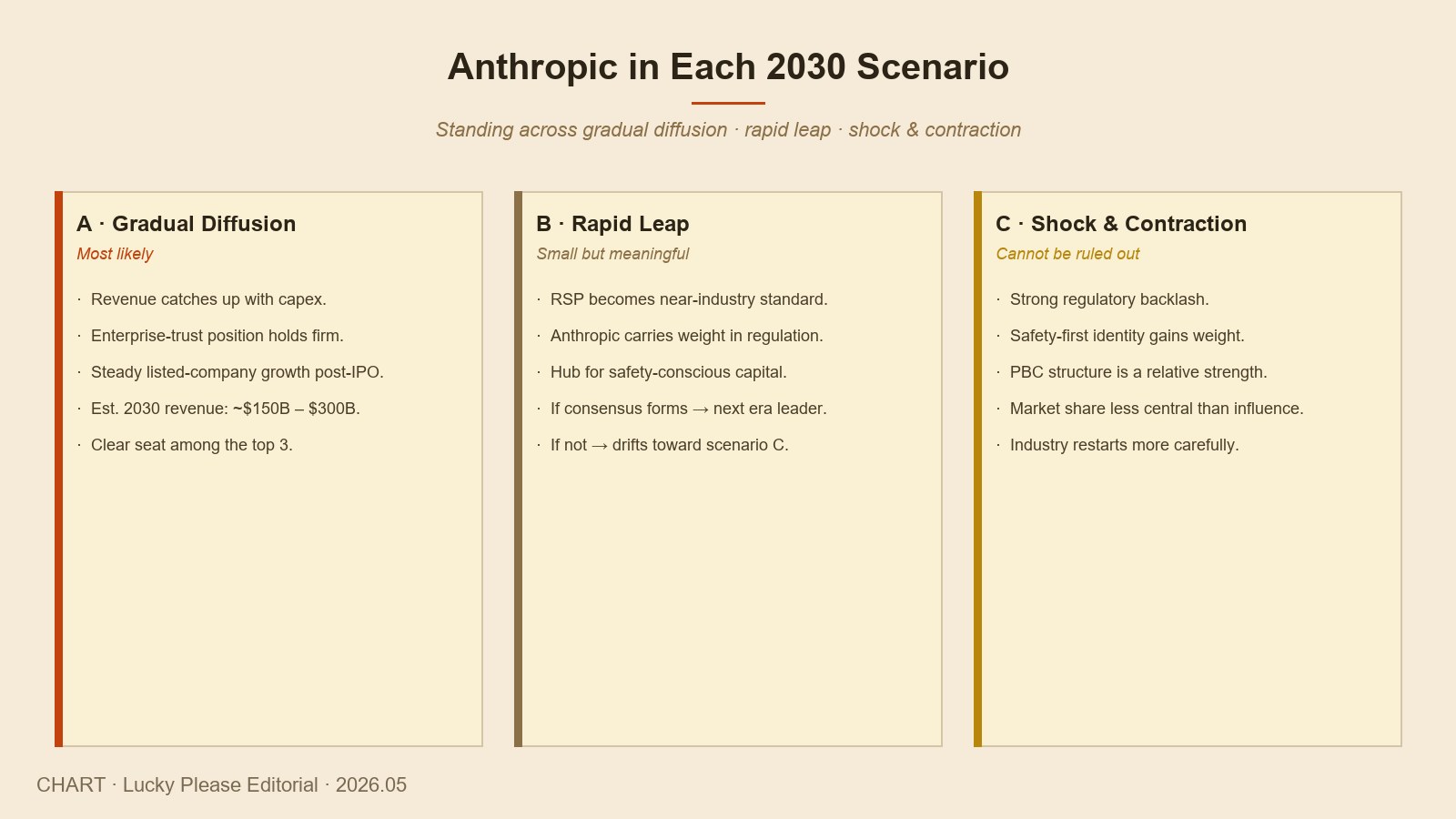

Next five years — Anthropic across three scenarios

Inside the three scenarios from Ep.6 — gradual diffusion, rapid leap, shock and contraction — we can place Anthropic's possible seat in each one.

Gradual diffusion scenario. Capability keeps improving steadily and industry revenue catches up to capex. Anthropic's strength inside this scenario is "frontier-level model + enterprise credibility." Steady revenue growth and post-IPO public-market continuation are most likely here. Market share stays clearly its own under the shadows of OpenAI and Google. Anthropic in 2030 could be a listed company with revenue in the ~$150B to ~$300B range.

Rapid leap scenario. The capability curve makes a steeper step up, into AGI or something near it. Anthropic's safety framework (RSP) likely moves into a near-industry-standard position. As social consensus forms around that step, the weight Anthropic carries in regulatory drafting becomes higher than its market share alone. If consensus does not form, however, this scenario drifts into Scenario C.

Shock and contraction scenario. A large incident occurs once, and strong regulatory backlash hits the whole industry. "Safety-first identity" becomes the firmest seat. As the OpenAI 5-day crisis showed how a structural weakness can be exposed under stress, a company with a tight governance and consistent identity starts from a structurally stronger position when the moment comes. Anthropic's PBC and RSP can hold it up here. Market share matters less than influence over the next phase.

In all three scenarios, Anthropic's seat is not weak. The financial firmness produced by the revenue curve and profitability. The governance firmness produced by the PBC structure. The identity firmness produced by Constitutional AI and the RSP. These three firmnesses work in the same seat regardless of which scenario plays out. The fact that all three live inside one company is the central reason spring 2026 Anthropic sits in a clearly different seat from the other five.

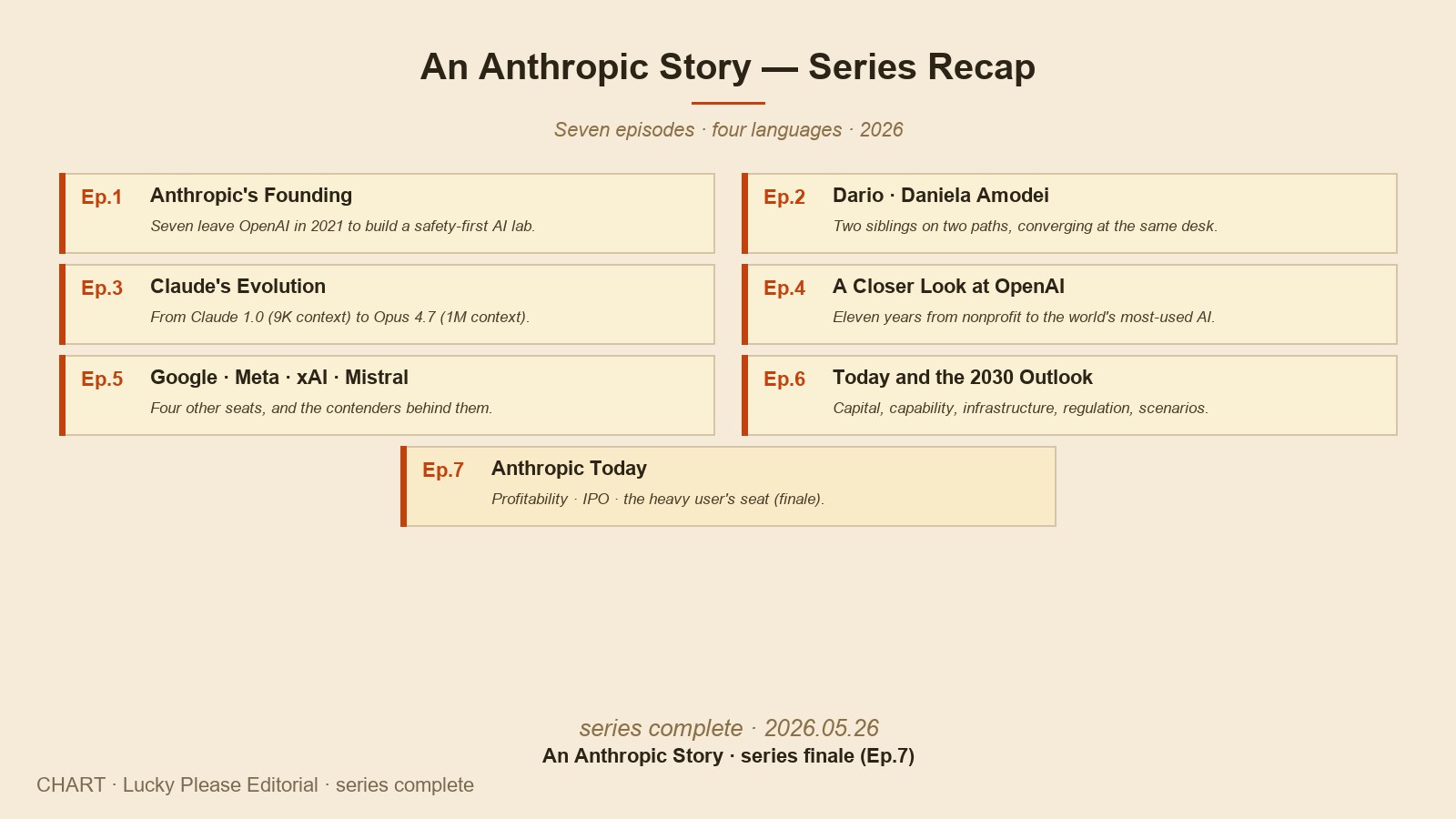

Seven episodes, on one page

Place the seven episodes on one page and one path becomes clear. Starting from a small office of one company, walking through every seat in the same industry, and returning to that company at the end. The same path, seen from seven different angles.

- Ep.1 — Anthropic's founding. The December 2020 office, the seat seven people left OpenAI for.

- Ep.2 — The Amodei siblings. Dario and Daniela's two paths converging at the same company over five years.

- Ep.3 — Claude's evolution. From the 9K-context model of spring 2023 to the 1M-context Opus 4.7 of 2026.

- Ep.4 — A closer look at OpenAI. Eleven years of the largest competitor who started at the same desk.

- Ep.5 — Google · Meta · xAI · Mistral. The other four seats, and the contenders behind them.

- Ep.6 — Today and the 2030 outlook. The industry's coordinates, $1T in capital, three scenarios.

- Ep.7 — Anthropic today. The closing chapter, returning to where the series began: profitability, IPO, and the heavy user's seat.

One question sat at the start of the series. "By whose decisions is the future of a powerful technology shaped?" Looking back across the seven episodes, the answer splits into two. First, the future is shaped by the balance among the different answers existing simultaneously inside the same industry (this is where Ep.6's ending arrived). Second, even inside those several answers, the answer of a company with a consistent identity and a firm structure carries more weight as time goes on (this is where Ep.7 sits). The two answers do not contradict each other. They work together.

The seat Anthropic holds in spring 2026 shows where those two answers meet. A company grown alongside the other five, while at the same time having built a distinct seat that the other five do not occupy. The fact that revenue profitability, the IPO seat, and a tool inside a heavy user's daily work all live together inside one company is one of the reasons this series can be closed in spring 2026.

At the actual closing of the series

The last line goes from the position of the editor making this series. The seven episodes began from the seat of one user holding one company's tool in hand every day and working with it. That the same user could use the same tool to write a series about the same company, and publish that series simultaneously in Korean, English, Japanese, and Chinese — that fact itself is a small picture of where AI sits in this period.

The picture is possible because two seats grew together. First, model capability has reached a place that meets the breath of one person's work. Second, the company building that model carries an identity and a structure that earn the user's trust. The first company where those two seats grew together is Anthropic, and that is the reason this series began in that seat and returns to it.

Over the next five years the landscape will shift sharply again. Which of Ep.6's three scenarios unfolds is unknowable. Whichever scenario unfolds, the seat of a user holding a tool in hand and working with it continues. From that seat, new essays will be written and new series will start. To the readers who followed this series in one breath, see you again, in the same seat.

An Anthropic Story · Seven episodes complete. Thank you.

References · Sources

- CNBC, "Anthropic on Pace for First Profitable Quarter as Revenue Surges", 2026.05.20

- Bloomberg, "Anthropic In Talks to Raise $30 Billion at $900 Billion Valuation", 2026.05.12

- Bloomberg, "Anthropic Nears $20 Billion Revenue Run Rate Amid Pentagon Feud", 2026.03.03

- Bloomberg, "Anthropic Tops $30 Billion Run Rate, Seals Broadcom Deal", 2026.04.06

- Bloomberg, "Anthropic's Revenue Run Rate Tops $9 Billion as VCs Pile In", 2026.01.21

- VentureBeat, "Anthropic says it hit a $30 billion revenue run rate after 'crazy' 80x growth", 2026.05

- PYMNTS, "Anthropic Hits $30 Billion Run Rate as Enterprise Demand Accelerates", 2026

- Sacra, "Anthropic — revenue, valuation & funding", updated 2026.05

- Anthropic, Constitutional AI (Bai et al., 2022), Responsible Scaling Policy v2 (2024.10)

- Delaware General Corporation Law, Subchapter XV — Public Benefit Corporations

- Lex Fridman Podcast #452, "Dario Amodei: Anthropic CEO on Claude, AGI & the Future", 2024.11

- Dario Amodei, "Machines of Loving Grace: How AI Could Transform the World for the Better", 2024.10

- The Information, "Inside Anthropic's IPO Preparation", 2026.04 – 2026.05 reporting