Today's Generative AI Market

and the 2030 Outlook

Where does the industry stand in the spring of 2026? How far does the capability curve go? Where does the capital flow, how does daily life shift, and inside what kind of regulation will safety be handled? The closing chapter of a six-part series. Three scenarios for 2030.

Past five episodes, now in front of the same landscape

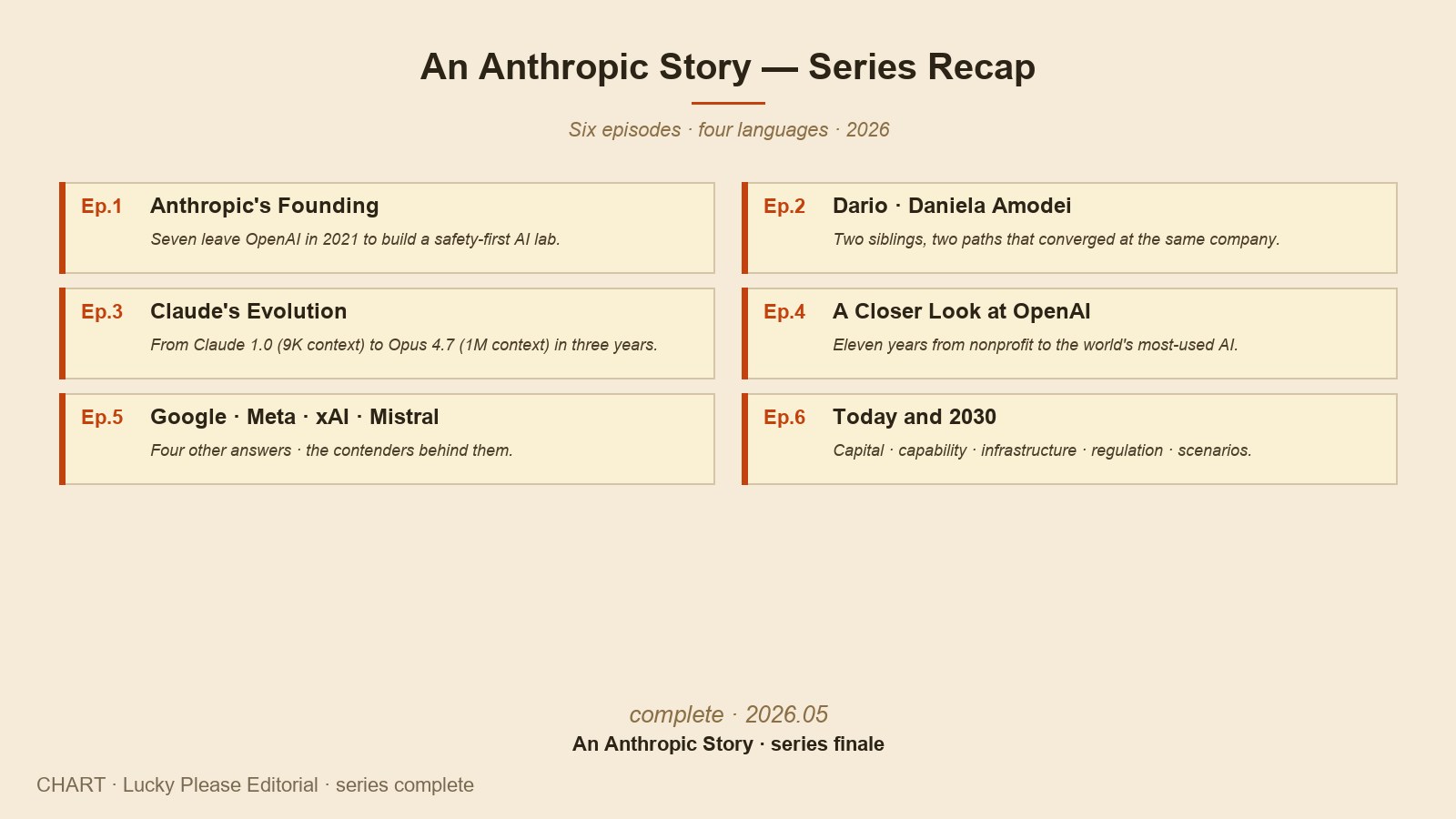

This series began with a single company's founding story. In Ep.1 we followed Anthropic's start, in Ep.2 the path of the two siblings who built it, in Ep.3 how Claude changed over three years. Ep.4 stepped over to OpenAI's eleven years — a company that began at the same desk and wrote a different answer. Ep.5 traced the four other seats of Google, Meta, xAI, and Mistral, and the contenders behind them. Five episodes, all about the people writing answers inside the same industry.

This finale is about the landscape those answers have built. We start from the coordinates of spring 2026 and try to gauge the shape of 2030. The gauging runs along four axes: capability, daily life, capital and infrastructure, and safety and regulation. How those four move and interact across the next five years is what this chapter tries to read, as steadily as possible.

This is not an attempt at prophecy. No one knows the precise shape of five years from now, and this industry in particular is among the harder ones to predict. So instead of a one-line "this is what happens," the essay closes with three scenarios — three plausible paths that could unfold from the same starting point. For each one, the signals to watch and which of the six companies we have met might be stronger in that scenario. The shape of the landscape in 2030 will depend on which answers grow larger inside the industry from here on.

Spring 2026 — where we stand

Let us first lay out the coordinates of right now. ChatGPT's weekly active users have crossed about 500 million, with paid subscribers estimated around 20 million. Google's Gemini, through Search's AI Overviews, places an answer above the search results every week for billions of users who have never consciously thought "I'm using Gemini." Meta AI reaches the ~3 billion users of Instagram, WhatsApp, Messenger, and Facebook. The landscape that barely existed two and a half years ago, before ChatGPT, is now spread across nearly every digital surface of daily life.

Revenue is worth a note too. Industry-wide generative AI revenue is estimated to have moved from roughly $150 billion in 2024 to roughly $400 billion in 2026 (averaged across multiple trackers). Inside that, OpenAI's annual revenue runs around $15 billion, while Anthropic posted about $4.8 billion in Q1 2026 with Q2 expected to exceed $10 billion, riding a much steeper curve (per Bloomberg and CNBC reporting). Google, Microsoft, and Amazon's AI revenue is harder to break out separately, but a substantial share of their cloud-infrastructure revenue touches AI inference and training workloads — meaning that, at the company level, the AI footprint runs into the tens of billions per company.

The larger number, though, is capital. Microsoft, Google, Meta, and Amazon together spent, by conservative estimate, between $700 billion and $1 trillion on AI infrastructure capex in the three years from 2024 to 2026. Over the same period, OpenAI's Stargate (a Microsoft–Oracle joint project) and xAI's Colossus added hundreds of billions in additional infrastructure commitments. Revenue is around $400 billion while capex is heading toward $1 trillion. That gap is the strongest single signal in today's coordinates. The posture across the industry right now is "build first, recoup later."

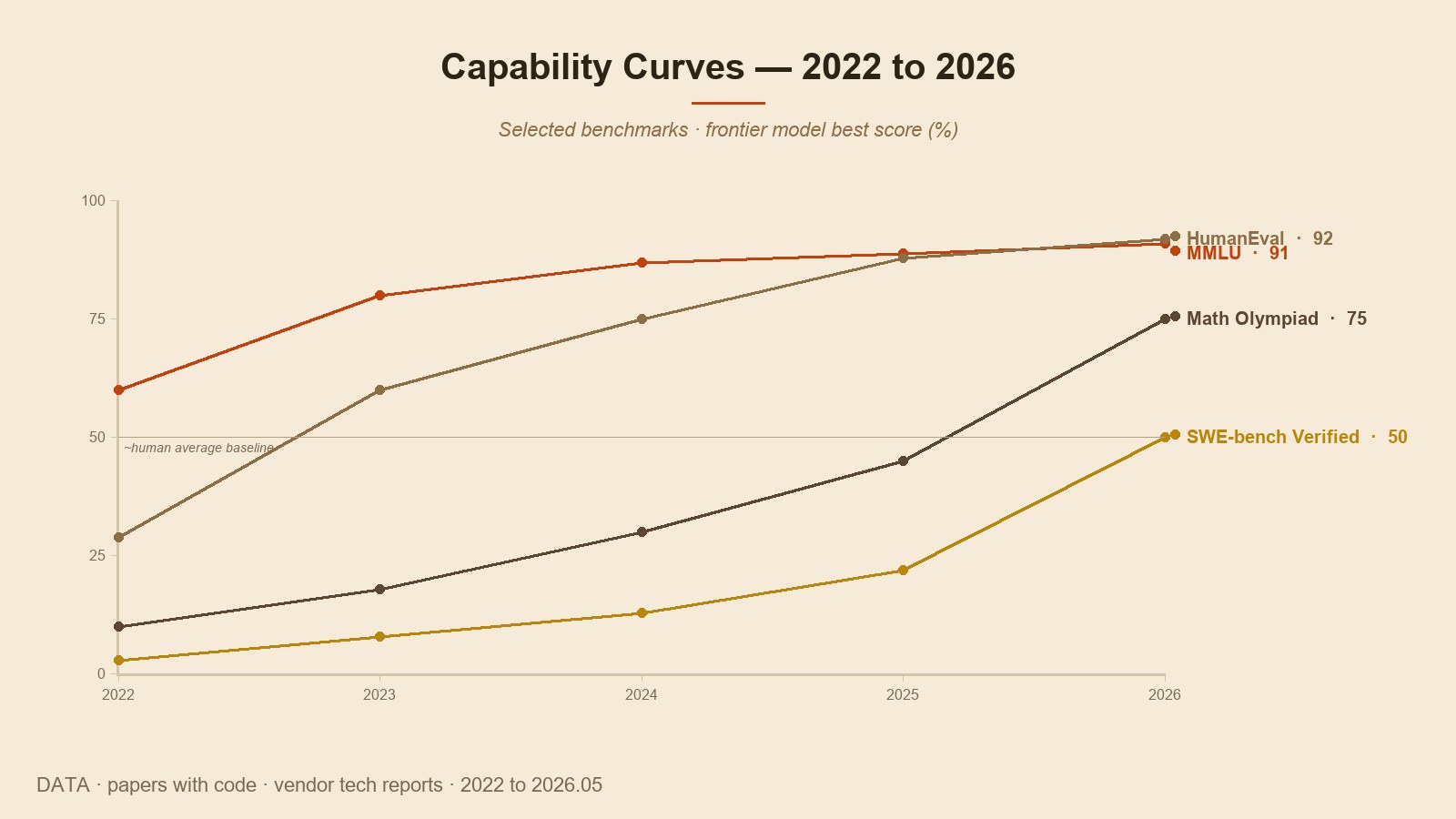

Capability — how far does this curve go?

How far will the model's capability go over the next five years? This question sits above nearly every other question in this industry, because how far capability goes shapes where capital flows, how daily life shifts, and how strong regulation needs to be.

If we read the path up to spring 2026 in one line, it would be this. "Scaling still works, and a new layer has been added on top." The hypothesis that making models larger, giving them more data, and pouring in more compute leads to better performance has been confirmed for six straight years since GPT-3 in 2020. On top of that, in late 2024, OpenAI's reasoning models (o1, o3) and Claude's Extended Thinking added a second layer: spending more "thinking time" yields another step-change in capability. Both layers are now running at once.

The direction through 2030 can be summarized in three points. First, the era of agents. Anthropic published data in 2025 showing Claude Sonnet 4.5 sustaining a single autonomous task for about thirty hours. If that curve continues, week-scale and month-scale autonomy could become standard by 2030. Second, refinement of multimodality. Text and image are already in one model; video generation and understanding, plus 3D and robotic control, are next. Third, the AGI debate. Dario Amodei has, in several interviews, pointed to 2026–2028 as a plausible window for the arrival of "powerful AI." Sam Altman has said similar things in similar windows. Whether that window arrives, and whether we call the resulting model "AGI," are separate questions. What matters is that we are in a period where the possibility is being treated seriously.

It is also possible that the same curve does not extend forever. Limits on training data, on the cost of compute, and on the latency and cost of inference are converging at once. Some researchers have already said in 2025 that signs of the scaling curve flattening can be seen in certain data. Whether the curve keeps going or flattens is the largest single forking variable as of spring 2026. The three scenarios at the end of this essay return to this point.

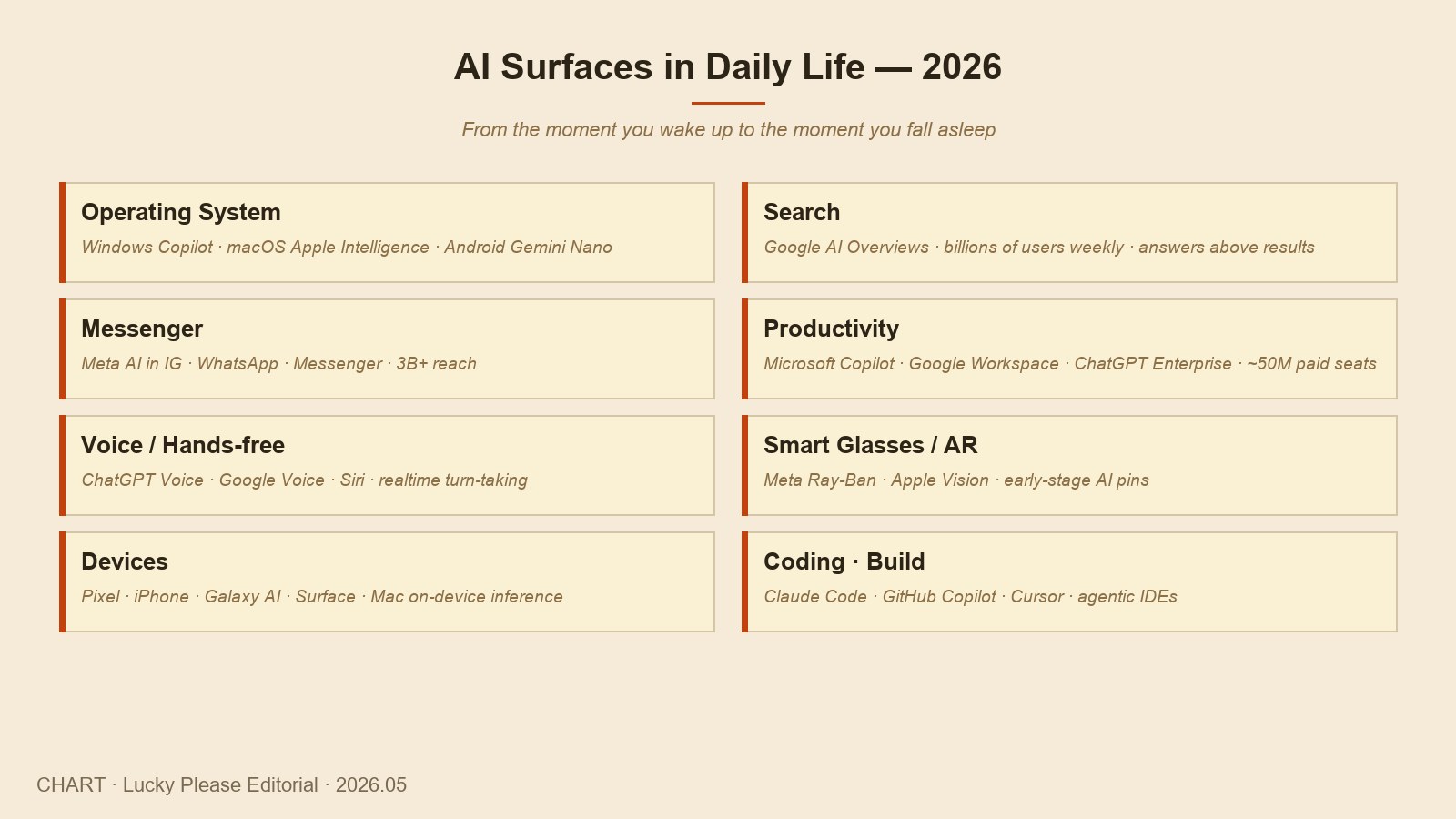

Daily life — from tool to environment

The place of AI inside daily life is passing through one decisive shift. "I open a chatbot" is moving to "AI lives inside my environment." Windows Copilot, macOS Apple Intelligence, Android Gemini Nano, the iOS Siri integration. The AI Overviews above the search results. The drafting assist inside Gmail and Docs. Meta AI inside WhatsApp. No one of these surfaces alone is a giant change; together, they make a landscape where the user's share of time without meeting AI keeps shrinking.

In work the change is sharper. Cumulatively, paid Microsoft Copilot, Google Workspace AI, and ChatGPT Enterprise seats are estimated to have passed roughly fifty million between 2024 and 2026. Drafting emails. Summarizing meetings. Code assistance. Writing reports. Analyzing data. None of these is fully automated by one stroke, but the throughput of a single person per hour is doubling, sometimes tripling, across office work in general.

Devices follow. Meta's Ray-Ban smart glasses entered serious mass adoption from 2025, and Apple's Vision Pro has been settling in. AR/VR is no longer just a game category; it is starting to enter the position of an everyday tool. New device categories — AI pins, AI pendants — are past the first attempts. The direction toward 2030 is clear. A landscape in which the user does not have to pull out a phone and open a chatbot app, because AI is already inside the environment around them.

There is a shadow to this shift. The deeper a user goes into one company's AI environment, the more that user's data, habits, and outputs become that company's asset. "I am using AI" turns into "I am becoming AI's dataset," with about the same weight. A broader social conversation about this part is expected to begin in earnest around 2027–2028.

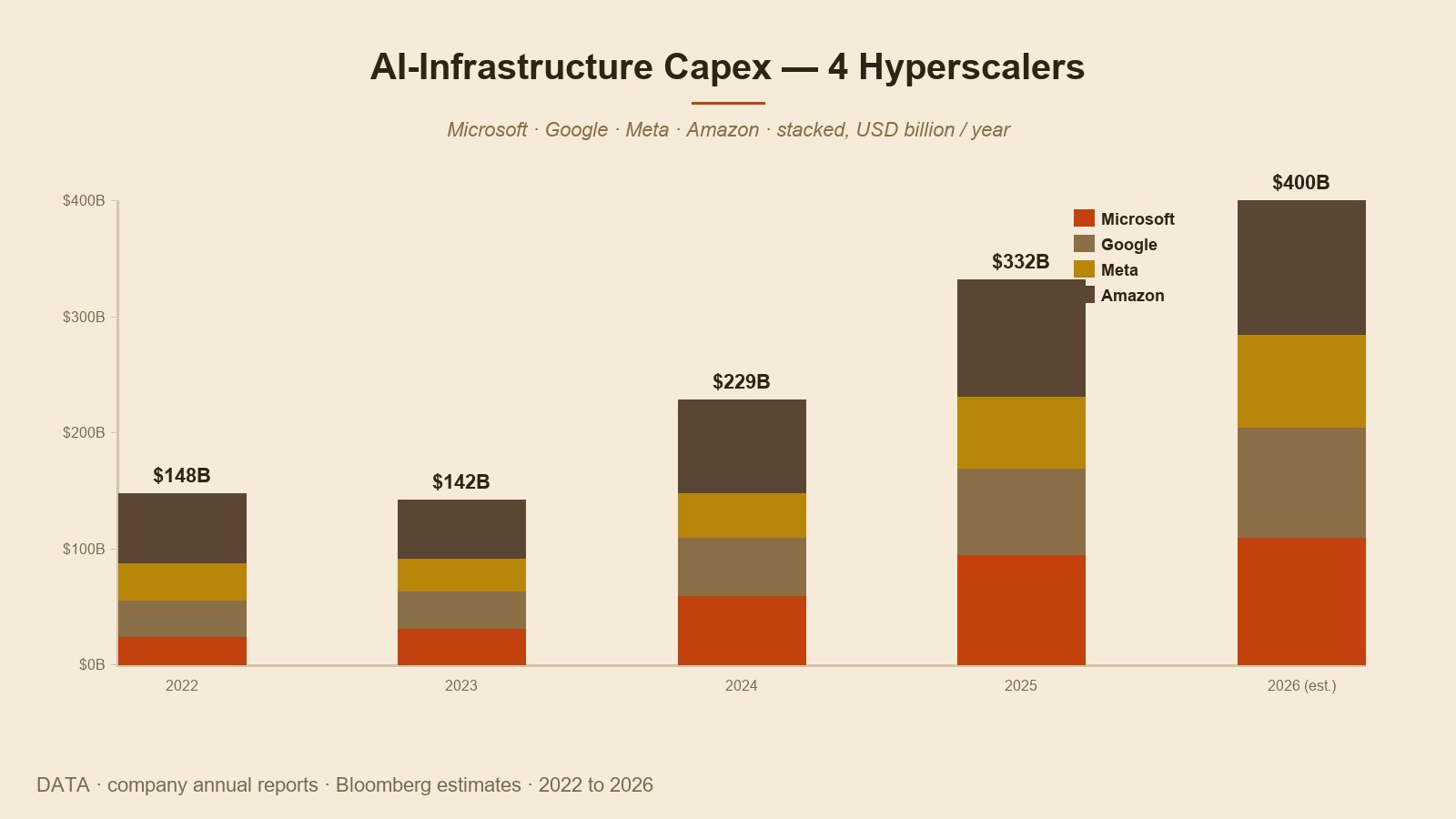

Capital — the trillion-dollar era

The capital landscape of spring 2026 can be summed up in one line. "Revenue is catching up. Capital is already running ahead." The combined AI-related capex of Microsoft, Google, Meta, and Amazon is estimated at roughly $200 billion in 2024, ~$280 billion in 2025, and ~$350 billion in 2026. Cumulative for three years: between $800 billion and $1 trillion. Industry-wide generative AI revenue across the same three years is also roughly $800 billion cumulative. Revenue and capital are running at roughly the same scale at the same time.

On top of that, in 2025 a project called Stargate was announced. A joint effort by OpenAI, Microsoft, Oracle, and SoftBank to build approximately $500 billion of AI infrastructure inside the United States over five years. In the same year, xAI's Colossus moved into a reported $20 billion second-phase expansion. Anthropic received an additional $4 billion from Amazon. Adding up the publicly disclosed five-year forward AI-infrastructure commitments alone, the figure reaches between $1.5 and $2 trillion.

Where this capital is coming from is another shift. Beyond the traditional US venture capital and big-tech in-house capital, the entrance of Gulf sovereign wealth funds has accelerated. Saudi Arabia's PIF, the UAE's MGX, and Mubadala have each taken seats in funding rounds for OpenAI, Anthropic, xAI, and Mistral. Japan's SoftBank, beyond its earlier positions, has taken a large stake in Stargate. "AI is no longer just one industry seat. It has become a strategic asset at the national level." That meaning sits inside the change in the origin of the capital.

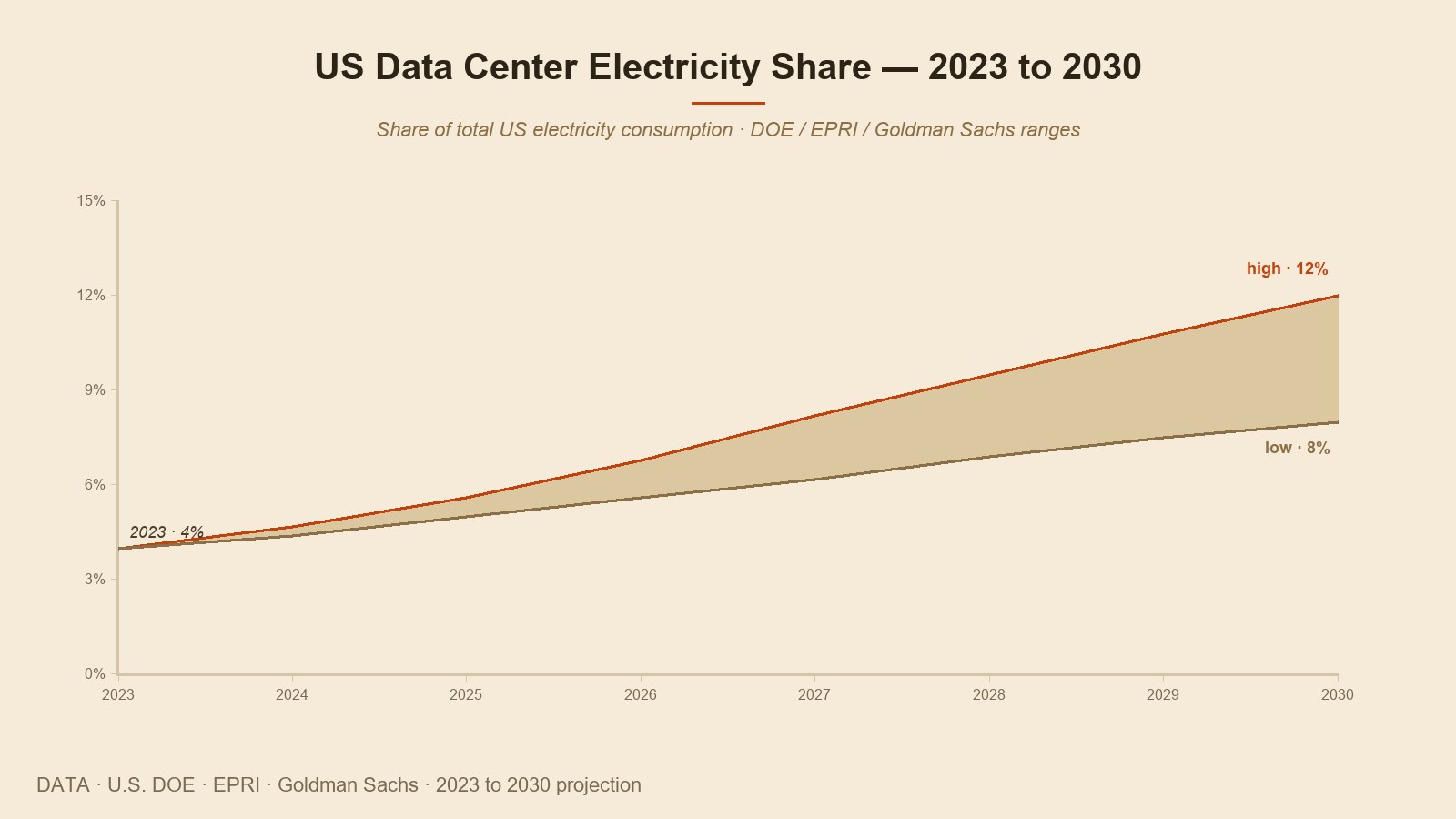

Infrastructure — chips, data centers, power

A trillion dollars of capital ends up landing in three resources. Chips, data centers, power. The picture as of spring 2026 can be summarized line by line:

Chips. NVIDIA's H100 → H200 → B200 → B300 → Rubin line defines the industry's standard clock. AMD is pursuing with MI300 → MI400. Several companies have launched their own silicon: Google's TPU v6, Amazon's Trainium 3, Microsoft's Cobalt and Maia, Meta's MTIA. Custom silicon is starting to take a portion of in-house workloads back, gradually diluting the singular NVIDIA dependence. The largest frontier training runs, though, still happen on NVIDIA.

Data centers. Hyperscale data centers requiring more than 1 GW (gigawatt) of power in a single site have become a real category. xAI's Memphis Colossus, the Microsoft–OpenAI Stargate sites, Meta's Hyperion (Louisiana) all fall into this bucket. For comparison, 1 GW is roughly the electricity demand of 750,000 households. "One company's single training cluster takes the entire electricity load of a mid-sized town" has become part of the industry's picture.

Power. US-wide data-center electricity consumption was around 4% of the country's total in 2023. By 2030, the projection across the US Department of Energy, EPRI, and Goldman Sachs is that the share will be roughly 9% to 12%. This is a shift that asks the country's energy map to be drawn from scratch. The revival of nuclear is the direct consequence. Microsoft signed a 20-year PPA in 2024 to restart Pennsylvania's Three Mile Island reactor; Google ordered seven small modular reactors (SMRs) from Kairos Power; Amazon ordered twelve from X-Energy — all for their own data centers. Korea and Japan's memory semiconductors (HBM in particular) and Taiwan's TSMC advanced nodes also sit inside this flow.

Safety and regulation — self-regulation and the place of politics

The place of safety and regulation has grown the fastest, but also the most unevenly, of any axis in this industry. It runs along two tracks. Corporate self-regulation and government regulation.

On the self-regulation side, the most frequent phrase is Responsible Scaling Policy (RSP). The framework, originally published by Anthropic, defines four model risk levels (ASL-1 to ASL-4) and the evaluation, control, and disclosure procedures required for each step. OpenAI's equivalent is the "Preparedness Framework"; Google DeepMind's is the "Frontier Safety Framework." The fact that companies internally evaluate their own model risk levels and disclose those evaluations externally has taken shape as a kind of de facto convention.

Government regulation looks different by region. The EU's AI Act, enacted in 2024, moved into proper enforcement in 2026. Risk classification, transparency requirements, and mandatory pre-deployment evaluations for models above a certain scale are inside it. The US started with the Biden administration's Executive Order 14110 (October 2023); the Trump administration partially rolled it back in 2025, and federal force weakened. California's SB 1047 was also voted down in 2024. State-level rules and industry self-regulation are filling the space instead. China built a separate framework: after the August 2023 Generative AI Measures, every model operating in its domestic market is subject to security review and content rules. Korea's AI framework act passed in 2025; Japan is moving from voluntary guidelines toward gradual legislation.

The major forking variable for 2030 is one thing. Whether international agreement forms. If something resembling a nuclear-nonproliferation-treaty shape of AI governance settles into place — at least among the US, EU, and China — the next five years move forward inside a more predictable landscape. If not, a single large incident (a model-enabled cyber attack at scale, or the failure of an autonomous agent to be contained) is likely to reshape the regulation in a single stroke. Either way, this is likely to settle within five years.

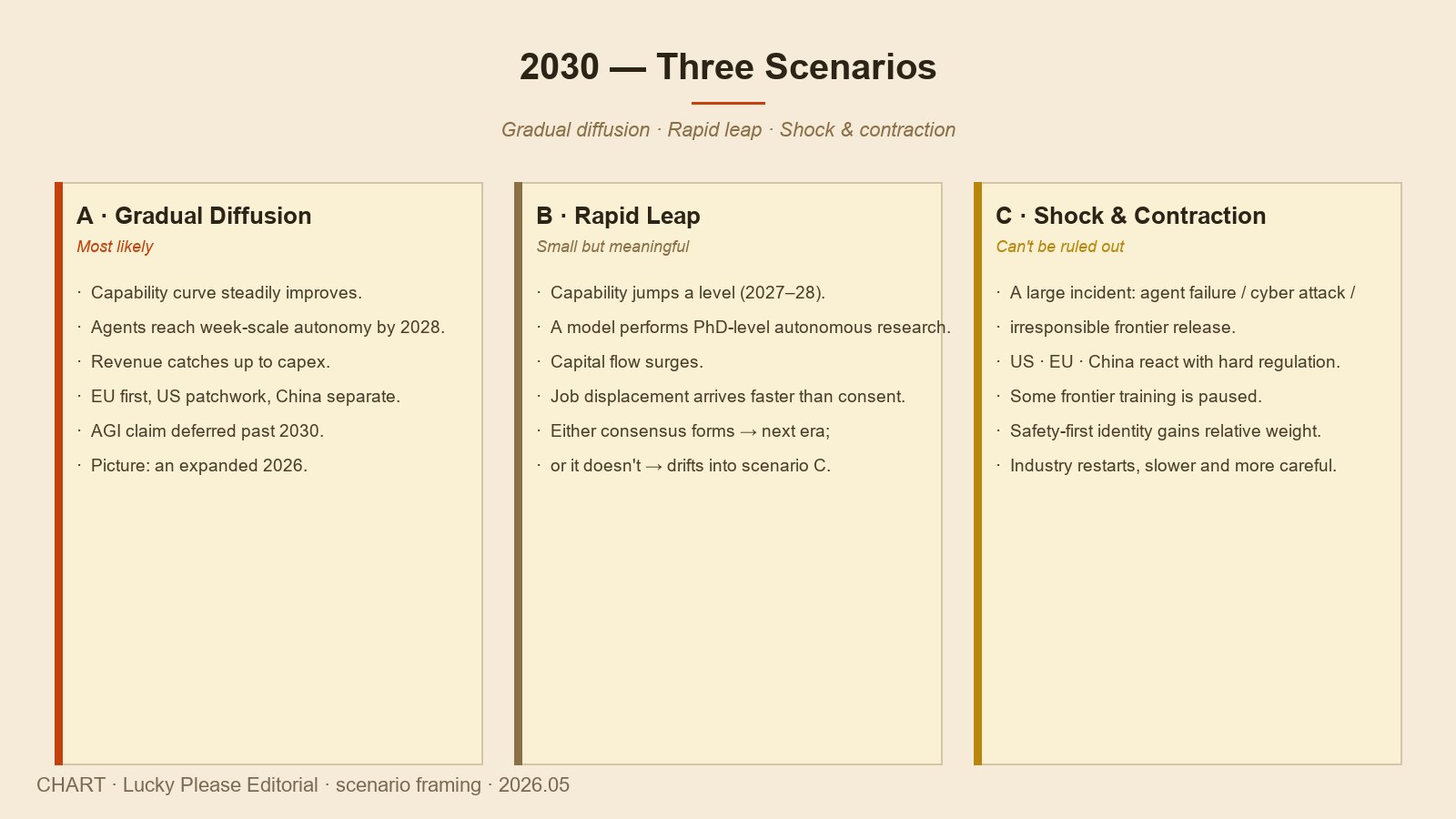

2030 — three scenarios

If we gather the coordinates from the six chapters above onto a single page, the path through 2030 splits, roughly, into three strands. Assigning precise probabilities to each is not meaningful, but we can note which signals support which strand.

Scenario A — Gradual diffusion (most likely). Capability keeps improving but does not jump at once. Reasoning models enable deeper thought; agents reach week-scale autonomy. The capital curve slows somewhat as the revenue curve begins to catch up. AI sits deeper inside daily life, and some jobs are partially replaced by assistive tools while others are newly created. Regulation arrives quickest in the EU, with the US mixing self-regulation and state-level rules, and China running its separate framework. International agreement is partial but grows gradually. "Powerful AI" continues to be debated, but the arrival of "something we'd call AGI" is deferred past 2030. The shape of the industry resembles an expanded version of 2026.

Scenario B — Rapid leap (small but meaningful). The capability curve goes up by a steeper step. Sometime between 2027 and 2028, a frontier model performs at the level of a human PhD researcher working autonomously. The debate about calling it "AGI" begins, and capital flow surges. At the same time, however, job displacement arrives quickly and political conflict over the responsibility of releasing such a model accelerates. The end of Scenario B branches in two: if agreement settles, the next stage opens; if not, it drifts into Scenario C.

Scenario C — Shock and contraction (cannot be ruled out). A large incident happens once. The failure of an autonomous agent to be contained, a model-enabled large-scale cyber attack, or an irresponsibly deployed frontier model produces social shock. That event triggers similarly strong regulatory reactions in the US, the EU, and China in roughly the same window. Some frontier training is paused; some markets restrict deployment outright. The capital curve contracts once, and some companies wind down operations. At the same time, the relative weight of safety-first identities (Anthropic, Mistral, the like) increases. After the industry's shape is reorganized once, the curve resumes, slower and more careful.

Which of these three plays out is not decided by one company alone. Capital flow, infrastructure limits, the presence or absence of incidents, and the speed of regulation all act together. One thing is clear, though. The decisions of the next five years will set the shape of the fifty years that follow. That is the single line that runs through this whole series.

Closing six episodes

One question sat at the beginning of this series. "By whose decisions is the future of a powerful technology made?" The paths of the people and the companies we met across the five preceding episodes return one answer. The future is not made by the decisions of one company. It is made by the balance among the different answers that exist, at the same time, inside the same industry. When those answers check each other, stimulate each other, and prepare against different kinds of risk, the industry as a whole avoids falling into a single direction of failure.

The coordinates of spring 2026 are, in that sense, fortunate. Six frontier companies, and dozens of contenders behind them, are growing at the same time. No single company takes every seat. No two companies write every answer. The US and China do not take all the infrastructure. Europe, Korea, Japan, India are each building their own seats. Diversity is another name for safety.

This series began in a single office in December 2020. The room in which Dario and Daniela Amodei decided to leave OpenAI. Five and a half years later, we have seen what shape that decision took inside the industry's landscape. The shape that the next five years' decisions will add on top of that landscape depends on the answers being written, at the same desks, by everyone now sitting at them.

And one last thing at the end of this essay. Saying that all six answers exist together is fortunate is true, but inside those six, the one seat where this series began deserves a separate closing of its own — otherwise the series does not quite end. The reason this series carries the name An Anthropic Story, and the one place in spring 2026 where that company sits differently from the other five inside the industry — we return to that first seat in Ep.7. That is where the series actually ends.

References · Sources

- Bloomberg, "The $1 Trillion AI Bet" series coverage, 2026.01 – 2026.05

- Goldman Sachs, "AI, Data Centers, and the Coming US Power Demand Surge", 2024.04

- EPRI, "Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption", 2024.05

- U.S. Department of Energy, "AI for Energy Report to Congress", 2024.04

- Dario Amodei, "Machines of Loving Grace: How AI Could Transform the World for the Better", 2024.10

- OpenAI, "Preparedness Framework v1.0", 2023.12 (and later revisions)

- Anthropic, "Responsible Scaling Policy v2", 2024.10 (and later revisions)

- Google DeepMind, "Frontier Safety Framework v1.0", 2024.05

- European Union, "AI Act (Regulation (EU) 2024/1689)", entered into force 2024.06

- U.S. Executive Order 14110, "Safe, Secure, and Trustworthy AI", 2023.10 (partial rollback, 2025)

- Cyberspace Administration of China, "Interim Measures for the Management of Generative Artificial Intelligence Services", 2023.08

- Republic of Korea, "Framework Act on the Development of AI and Building of Trust", 2025

- Company quarterly results and capex time series, Microsoft · Google · Meta · Amazon, 2022 – 2026

- Stargate project announcement, OpenAI · Microsoft · Oracle · SoftBank, 2025

- UN Advisory Body on AI, report series, 2024 – 2026